Estate Planning Explained: How to Begin

Estate planning is one of the most critical components of a truly comprehensive financial plan. However, the process can be daunting, especially if you don’t have an estate plan or haven’t updated it. In such cases, meeting with a fee-only CERTIFIED FINANCIAL PLANNER™ Professional can provide a sense of relief, knowing that you are in capable hands.

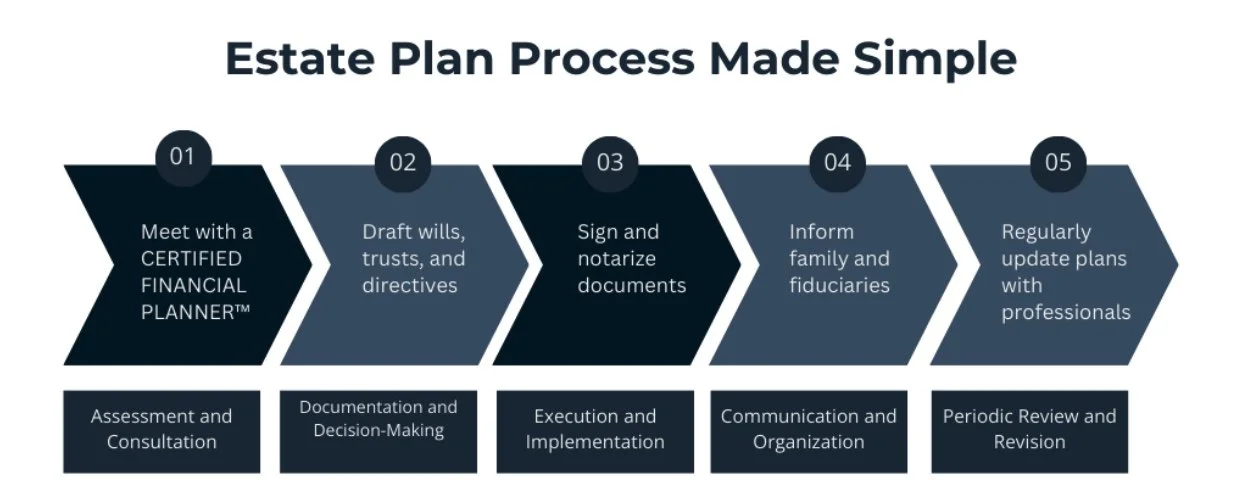

Let’s look at how to get started with an estate plan.

Everyone Needs an Estate Plan

Even if you don’t have a significant amount of assets, you need an estate plan. The bottom line is that every adult, regardless of age and level of wealth, can benefit from an estate plan.

After all, most people own an automobile, have a bank account, and have life insurance and/or investments. Estates consist of each of these assets along with real property. However, estate planning extends well beyond mere possessions.

Truly comprehensive estate planning also involves putting the proper procedures in place to prepare for the roadblocks ahead in life, such as illness, incapacity, and eventually passing away. For instance, if you were to become incapacitated, who would manage your finances and make healthcare decisions on your behalf? With the right estate plan in place, you will rest easy knowing you have done everything possible to ensure your loved ones can maintain their current living standard after your death.

Estate Planning Begins With a Will

Your will is one of the most important components of your estate plan. Your will designates the specific heirs that receive your assets. An executor is named in the will, providing you with the opportunity to carefully select a trusted individual with the responsibility and power necessary to distribute your estate as you desire and also pay debts on your behalf.

If you fail to establish a will, your property will be transmitted to surviving family members in accordance with the state’s intestacy laws. This can prove to be a challenging scenario, as the last thing you want is for the court to determine how your assets will be divided.

Revocable living trusts are available to shift property to loved ones after death. Living trusts bypass the dreaded probate process, meaning a court will not determine who receives your assets. The probate process can be lengthy and public - allowing, potentially, for third parties to make claims against your estate.

It also makes sense to establish a trust to protect assets you choose to leave to heirs. When creating a trust, you can select a trustee who will adhere to your specific instructions for managing your assets. This is especially important if you leave assets to young beneficiaries, or someone who may not be financially savvy.

Choose Your Beneficiaries

You worked hard for your money, so you should seize the opportunity to name specific beneficiaries. The beneficiaries you designate will receive your assets exactly as you desire. Whether you want to leave your car to your son, your cottage to your daughter, or your investments to your spouse, now is the time to make those decisions and select beneficiaries as appropriate. This sense of control over your assets can be empowering.

Be sure to consult with a CERTIFIED FINANCIAL PLANNER™ Professional during this process to ensure the value of your assets is accurate and updated. This will set the stage for those assets to be distributed exactly as desired.

Estate Tax Mitigation

If you aren’t careful, the government could receive a sizable chunk of your hard-earned money when you depart. Your CERTIFIED FINANCIAL PLANNER™ Professional’s assistance will prove invaluable in helping you reduce your estate tax burden.

A CFP ® can explain the use of exemptions, such as the lifetime gift tax exemption, and how unused exemptions can be transferred to a surviving spouse, in the context of estate planning. Proper tax mitigation planning has the potential to save your relatives and other beneficiaries thousands or even tens of thousands of dollars.

Durable Power of Attorney and Advanced Healthcare Directives

Estate planning is not strictly limited to providing care for survivors. Estate planning also ensures a trusted individual can manage your finances through a durable power of attorney should you become too ill or incapacitated to do so yourself. It is also in your interest to establish an advanced healthcare directive that selects a healthcare agent to make decisions on your behalf when you are nearing death and too sick to verbalize your desires.

Organizing Paper and Digital Files

As is often said, the devil is in the details. If your paperwork or digital files are a mess, doling out your assets upon death will prove much more challenging. Do your loved ones and other beneficiaries a favor by organizing these files today.

A fee-only CERTIFIED FINANCIAL PLANNER™ Professional will help you get all the necessary paperwork in the proper order so your family doesn’t have to piece together the puzzle of your accounts, assets, and other estate-related documents after you pass away. Now is the time to organize the documents your executor will require to smoothly shift your assets to selected beneficiaries.

For example, it will certainly help if you provide your insurance policies, pension paperwork, bank statements, burial plot deed, and paperwork pertaining to investments to your executor as soon as possible. Continue to update your asset list along with the names and contact information of professionals who help you with your estate planning. Make sure your executor can easily access your information.

Paper documentation is certainly important, yet digital documentation and assets also matter a great deal in the context of comprehensive estate planning. Do not overlook your digital assets. If you have web-based stock trading accounts or other digital accounts, maintain a list of those accounts along with your usernames and passwords so your executor can access them easily.

Review Your Estate Plan Every Half-decade

Estate planning is dynamic rather than static, meaning it will change over time. Major life events such as a spouse’s death, divorce, marriage, and retirement have the potential to significantly change your estate plan.

Furthermore, Congress has the potential to alter estate tax law, so it is in your interest to meet with your fee-only CERTIFIED FINANCIAL PLANNER™ Professional and estate planning specialist at least once every half-decade to update your assets and related estate planning paperwork. This regular review and update process can provide a sense of security, ensuring your assets are distributed exactly as desired.

Contact Us

Ready to take the first step toward securing your family’s future? Contact us today to schedule a consultation with our team of fee-only CERTIFIED FINANCIAL PLANNER™ Professionals. Let us help you navigate the complexities of estate planning and build a comprehensive financial plan tailored to your needs and goals. Your peace of mind starts here.