Cash Flow is King

When we think about retirement, images of a gray-haired guy with a fishing pole on a lake come to mind. But, in addition to more time outdoors, it represents a new way to pay for our daily lives. Society has trained us to “save, save, and save some more” for decades. As fee-only financial advisers, we’ve found that it’s tough for people to spend their life savings. So, how do we create a mind shift?

Budgeting is Essential for EVERYONE

Assuming you know what you want to do in retirement – travel, get a part-time job, be a mentor, or take classes – it’s time to figure out how to pay for your dreams! Setting a budget is crucial, even if you haven’t done this since you were a newlywed. Due to the length and severity of retirement, you must dive deep into your lifestyle. It’s easier to make income and expense changes while you still have a job instead of course-correcting in your 80s or 90s.

Create a budget by looking at your life right now. We can provide a great template to help you start. This budgeting process isn't about restricting your spending but empowering you to make informed financial decisions and giving you the freedom and flexibility to enjoy your retirement to the fullest.

Recognize that certain expenses may change, but others may not. For example, you might think your spending on lunches will drop to zero – but that might not be the reality if you have more free time!

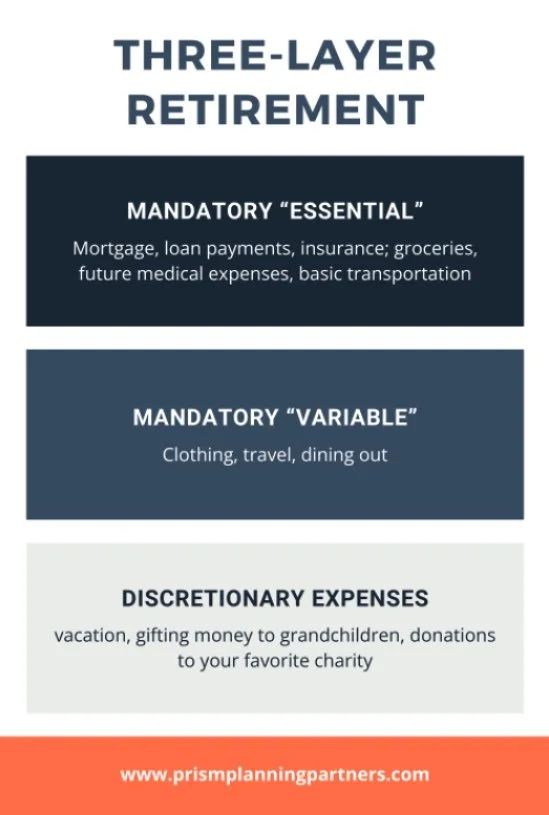

Three-Layer Retirement

At Prism, we think about budgeting in a slightly different way than most. Yes, we still think some expenses are “mandatory” and others are “discretionary.” But, when you’re saving for the retirement you really want, it helps to add a layer to the “mandatory” column. We refer to retirement expenses as Essential, Variable, and Discretionary. Essential and Variable expenses take care of you (and are “mandatory”), whereas we think of Discretionary expenses as how you can help others more substantially.

Mandatory “Essential” and Mandatory “Variable”

Essential expenses include items like:

your mortgage

loan payments

insurance; groceries

future medical expenses

basic transportation

Variable expense examples include:

clothing

travel

dining out

Determine if an expense is essential or variable by asking: If I had a major financial loss, what expenses could I not live without? Shelter, gas, groceries, and insurance are essential. A variable mandatory expense is a non-extravagant extra. These expenses could be “cut” if necessary.

Thinking about expenses in these terms helps create two “floors” for your retirement paycheck. A floor means that, regardless of external forces, you’ll receive a specified amount of income intended to cover essential and variable needs.

Discretionary Expenses

Discretionary expenses compose the third layer of our retirement cake. These are additional expenses above and beyond what you currently spend. Some examples include:

taking the entire family on a fun vacation

gifting money to the grandchildren

making extra donations to your favorite charity.

Say we determine that you currently spend $80,000 per year as a working couple and would like to spend an additional $20,000 per year in retirement pursuing a travel blogging dream. We’d first divvy up the $80,000 into essential vs variable expenses. We then determine that essential expenses are $50,000, and variable are $30,000. The first “layer” of your cake to protect are your essential expenses, then $30,000 of variable, and finally, $20,000 of discretionary expenses.

Recreating your “Paycheck”

Before resigning from your career, it’s important to understand your future resources. This process is often referred to as 'recreating your paycheck' in retirement, where you structure your income to cover your essential and variable expenses, and potentially leave room for discretionary spending. This includes guaranteed retirement income sources (such as a pension, social security, or annuity), as well as what your savings can generate for you (e.g., how much can I take out of my 401(k) ongoing?) Some folks like to make sure their guaranteed income sources perfectly cover essential and variable expenses. Others do not want to tie up too much of their savings for this guarantee. Both methods have pros and cons, and it’s important to meet with a fee-only adviser and generate a plan to figure it all out!

Cultivating a Retirement Mindset

Transitioning into retirement involves more than just envisioning leisurely days by the lake; it’s a fundamental shift in both time management and financial strategy. Despite an emphasis on “save, save, save!”, many find it challenging to spend their accumulated wealth when the time comes. To facilitate this mind shift, budgeting is essential, even if you are already financially successful. By categorizing your expenses, you can structure your retirement income to cover both your needs and aspirations.

Contact Us

Does this mind shift sound interesting to you? Would you like to receive our budgeting template?

Feel free to contact us, and we’d be happy to talk!